Start with the Numbers

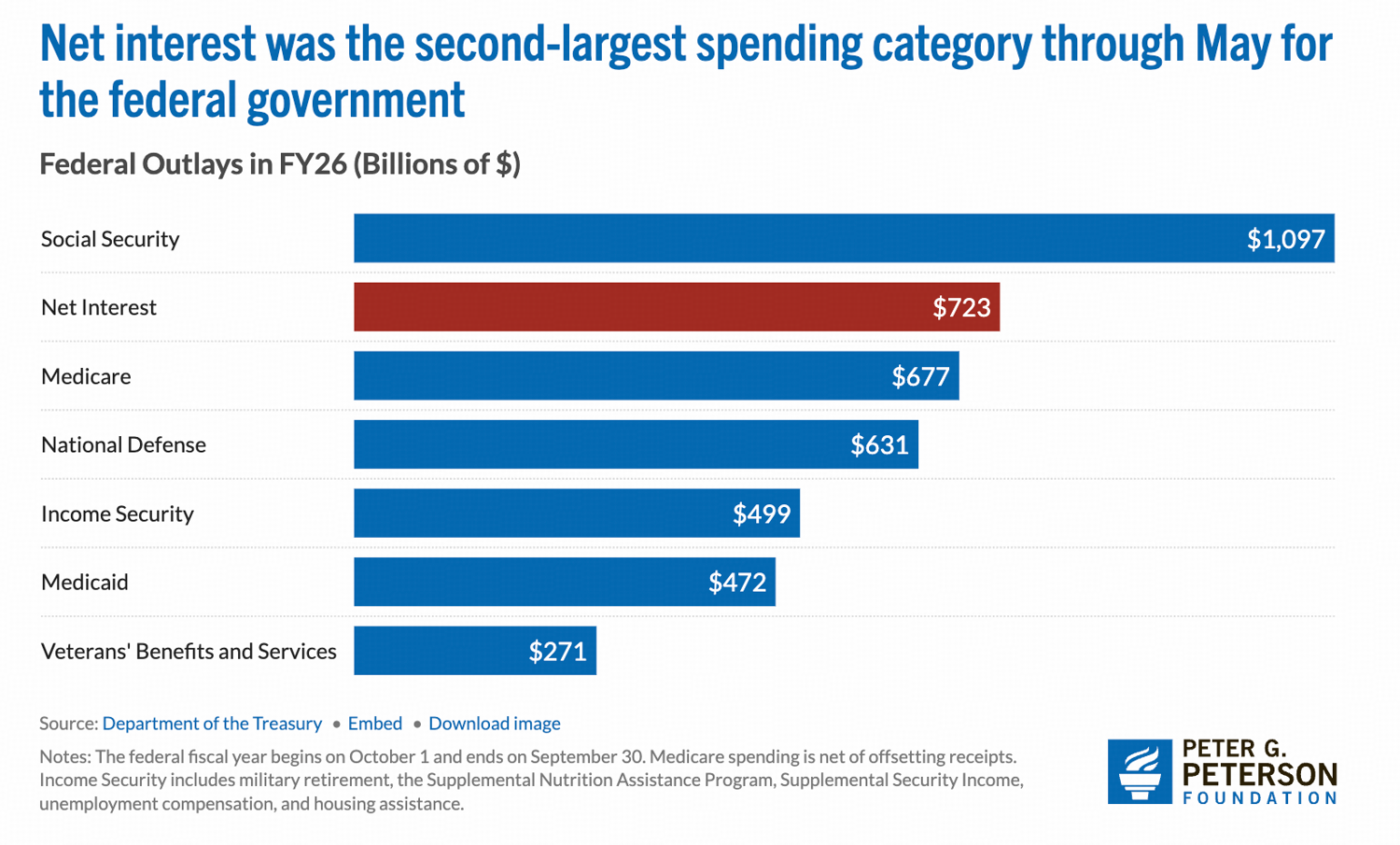

Federal debt is around $39 trillion. Net interest on that debt is now running over $1 trillion a year, about 3.3% of GDP. The rapid accumulation of federal debt, in addition to higher interest rates on that debt (relative to longer-term rates that existed just a few years ago), has pushed up the federal government’s cost of borrowing. Interest costs so far in FY26 have been the second-largest spending category for the federal government, outpacing outlays for all budget categories except for Social Security.

The debt doesn't reprice all at once. It rolls over gradually, as old securities mature and get replaced at whatever the going rate is. But over the full refinancing cycle, every 100 basis points of higher funding cost adds roughly $390 billion to annual interest expense. This is a permanent addition to the deficit, year after year, that itself has to be financed with more borrowing.

Since COVID, the U.S. has shifted financing heavily toward T-bills: in 2025, 84% of government debt issuance was made up of Treasury bills with maturities of 12 months or less, the highest ratio since the financial crisis.

T-bills now represent 22% of all outstanding marketable Treasury debt, above the historical 15–20% target range the TBAC has historically recommended. By issuing fewer 10Y and 30Y bonds, the Treasury reduces the volume of long-duration supply that must be absorbed by price-sensitive buyers, relieving upward pressure on long-end yields.